- Budgeters Anonymous

- Posts

- How Parents Can Start Investing in 2026

How Parents Can Start Investing in 2026

Time is more important than money

Daniel Brigham

December 07, 2025

You Owe It To Your Family

Becoming a parent flips your world upside down.

Suddenly, the future feels closer, scarier, and more expensive than ever.

But here’s the good news:

You don’t need a six-figure income to build wealth for your family.

You just need a plan, a few simple accounts, and consistency.

And you can start with as little as $100 per month.

Below is the exact blueprint I recommend — one that can scale as you start to have more income available.

Your Investment Starter Plan

The $100/Month Starter Plan

Here’s how to divide that first $100:

$20 → 529 Plan (kids college)

$40 → Roth IRA (your retirement)

$40 → High-Yield Savings Account (HYSA) (your emergency fund)

And every year, you increase your monthly total:

Year 1: $100/mo

Year 2: $200/mo

Year 3: $300/mo

Year 4: $400/mo

Year 5: $500/mo

This slow ramp-up protects your budget, especially when you’re already adjusting to the added cost of childcare and diapers.

Let’s break down each account, why it matters, and how much it can grow.

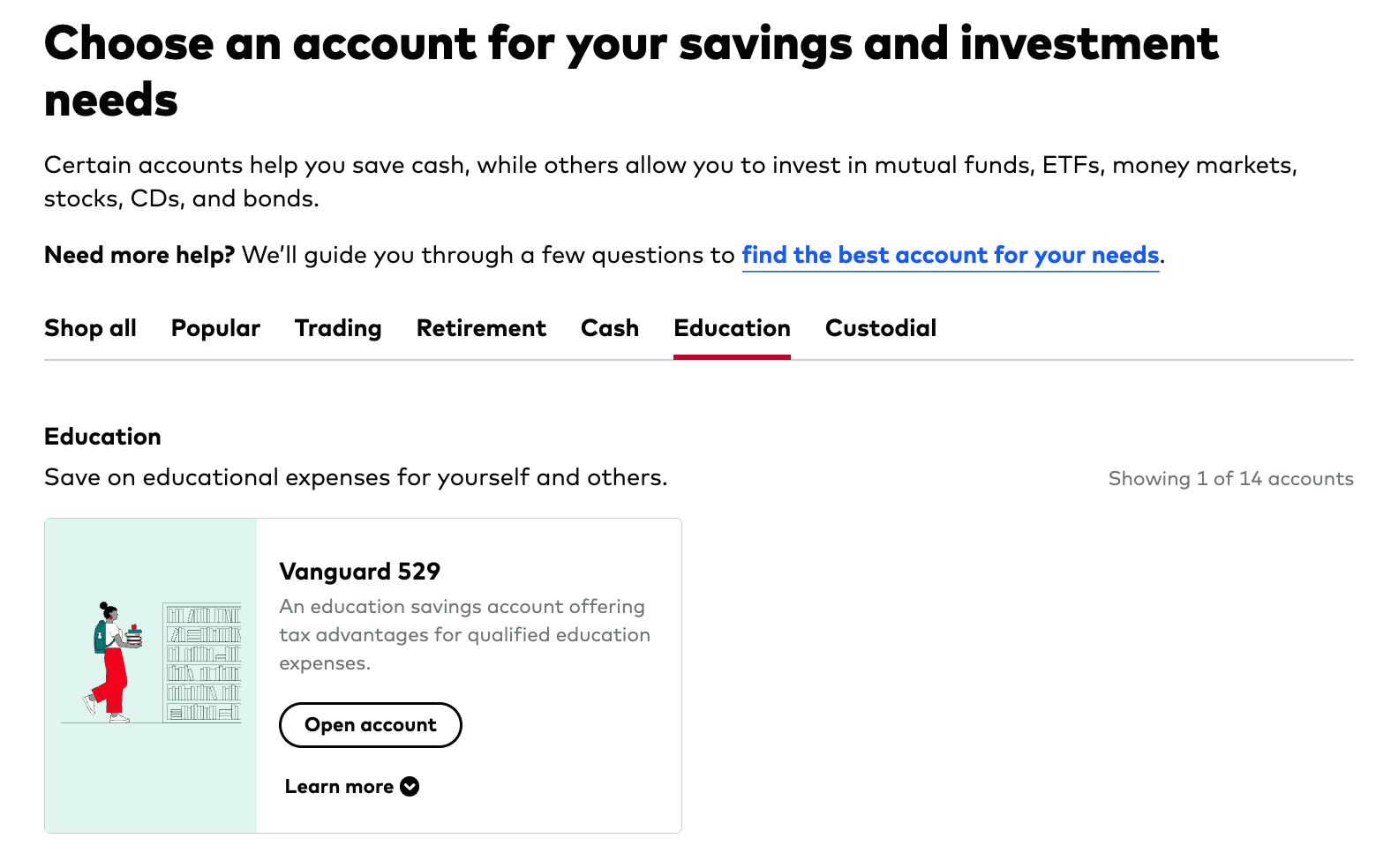

The 529 Plan

A 529 plan is an investment account designed for education expenses like:

College tuition

Trade school

Certain K–12 tuition

Books, supplies, room & board

Even student loan repayment

Why it’s amazing:

Your money grows tax-free.

Withdrawals for education are tax-free.

Many states offer tax deductions or credits.

You can rollover $35k to a Roth IRA for your kid if they don’t use it.

What $20/month can become:

Unlike a savings account, you can invest this money into the stock market - Averaging 7%/yr

$20/mo at 7% for 18 years grows to ~$9,300.

Increase it slowly each year (as our 5-year plan does), and you could easily hand over $50k+ to your kid for college.

The best place to open one of these is where you already have your IRA.

You’re looking for something like this.

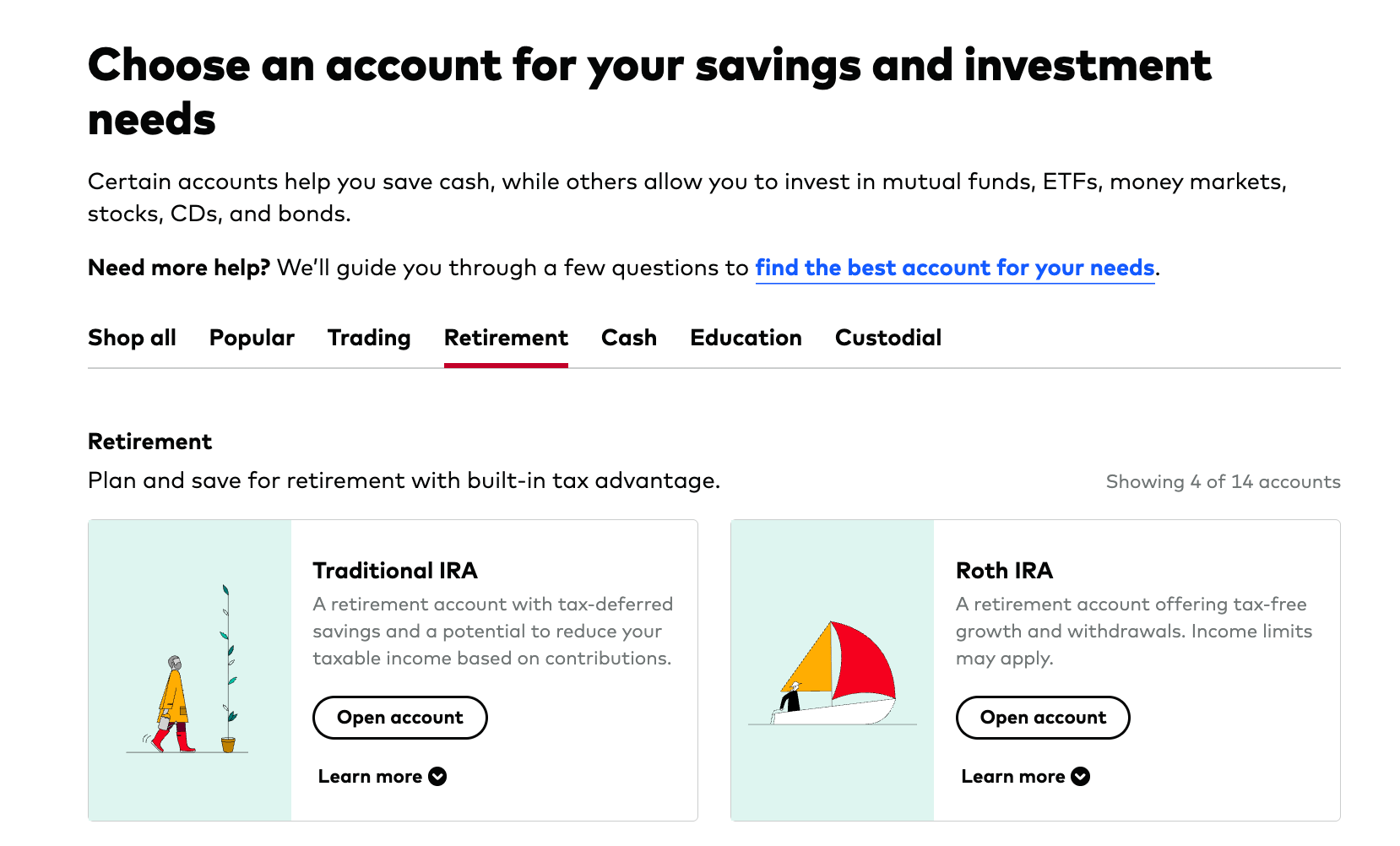

The Roth IRA

Your retirement matters even more now that you're a parent.

A Roth IRA lets your money grow tax-free for decades and come out tax-free at retirement.

Why it’s powerful:

You contribute after-tax dollars, so future withdrawals are tax-free.

You can also withdraw your contributions (not gains) anytime for emergencies without penalty.

It’s one of the best vehicles available to the middle class.

What $40/month can become:

At a 7% return:

After 18 years → ~$17,500

After 30 years → ~$48,000

After 40 years → ~$101,000

And remember: this is just starting with $40/mo and slowly ramping up.

For example: $500/mo for 30 years leaves you with $600k+

Parents who stay consistent—even at small dollar amounts—win big over time.

You’re looking for something like this.

The HYSA (Emergency Fund)

This is your safety net.

Goal balance: 3–6 months of living expenses

Why it’s important:

Kids get sick

Cars break

Jobs change

Life punches you in the face every few months

A HYSA right now can ear around 3-4% interest, which keeps your emergency fund from losing value to inflation.

Following the blueprint I proposed would give you about $20k after 10 years.

Once you hit 3–6 months of expenses, you would redirect that money straight into the Roth IRA, accelerating your long-term growth.

I know 10 years can feel like a long time to build an emergency fund, but again, you’re starting from a place where you’re saving $10 per week.

Final Encouragement

If all you can do is $100/month, that’s ok, you need to start somewhere.

Every financially stable parent you know started small.

Your first contribution might feel tiny, but what it represents is huge:

A decision to build a different financial future for your family.

You don’t need perfection.

You just need to start.

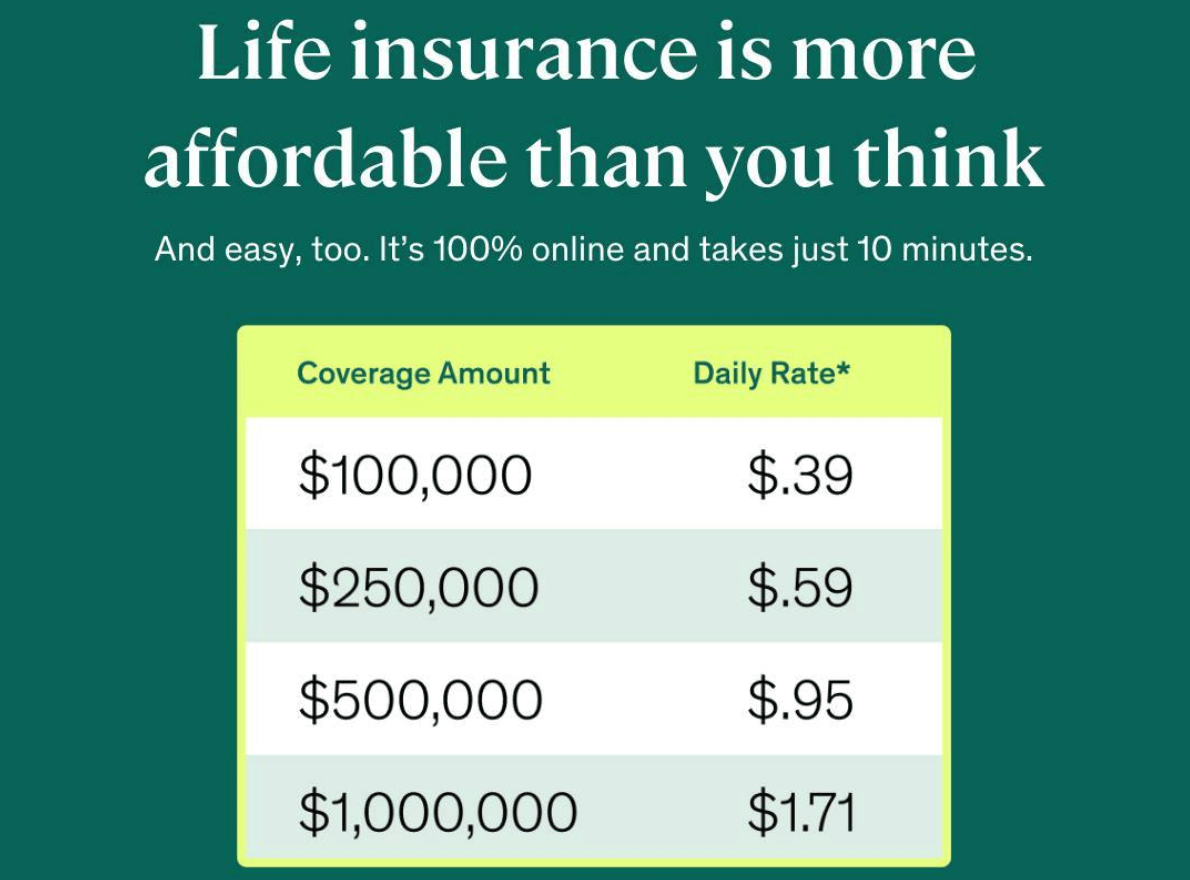

And to bulletproof this plan, I highly recommend getting life insurance.

Term Life insurance is income protection in case something happens to you.

Because your little one is depending on your income.

Most parents are good at getting $500k-$1m in coverage across a 20-30 year term.

I recommend Ethos just because you can get signed up in ten minutes without seeing a doctor.

That’s it for this week.

As always, let me know if you have any questions.

Dan

Reply